Read this blog to learn how retail medicine, a once disruptive healthcare business model, is now in acceleration mode with new variations (pivots) of the model still coming to market.

The team at imagine.GO are experts in the field of retail health. Since 2005, we have helped bring to market over 200 retail health facilities and stores for companies like RediClinic, Smartcare, The Little Clinic, HMSA, Affinity Health Plan, United Healthcare, and others. We have helped our clients develop their retail strategy, design and launch their retail channels, and build retail staffing models.

Big and Getting Bigger

According to the Urgent Care Association of America, the number of walk-in “retail” clinics across the country is now over 9,400. That is a 20 percent increase since 2009. Why is that? We believe one of the reasons is the Affordable Care Act. There are now over 10 million newly insured consumers seeking health care services through primary care channels that are already over capacity. So now the demand is being orchestrated through these retail medicine outlets. So what is the distinction between these retail medicine channels?

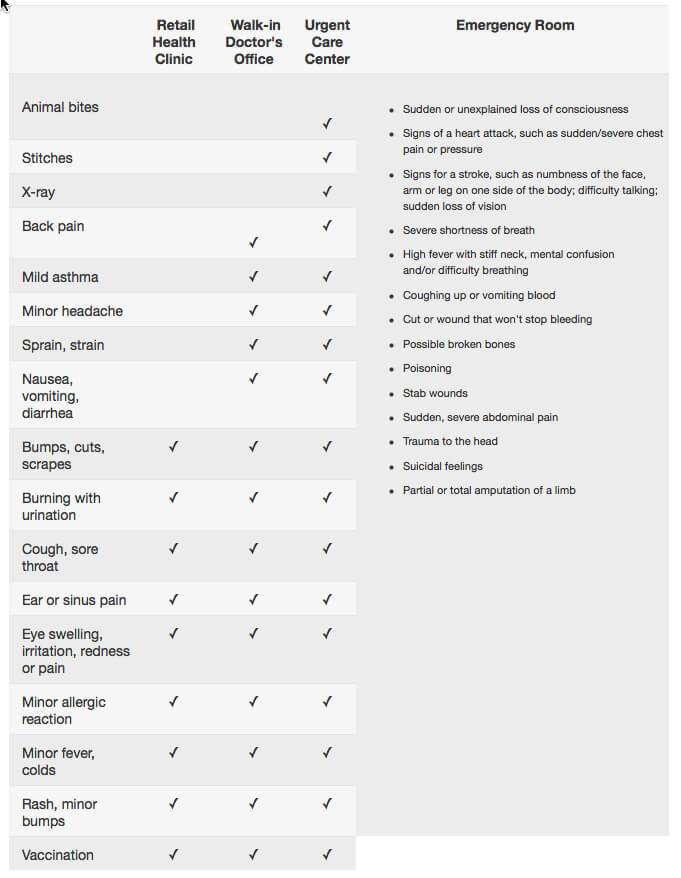

Retail Clinics are Nurse Practioner staffed walk-in health facilities located in retail stores, supermarkets, and pharmacies. They treat lower scope ailments and minor illnesses, as well as provide preventative health care services.

Urgent Care Facilities staff Physicians and Nurse Practitioners. They are walk-in health facilities that are usually free standing to treat health problems that require immediate attention but are not life-threatening. Some examples include setting broken limbs, adding and removing stitches, and even giving x-rays.

Walk-in doctor’s offices are Physician staffed walk-in health facilities that do not require visitors to be existing patients. They provide simple medical care in a hurry and treat problems such as mild asthma or minor allergic reactions.

An example of the services that each channel provides is shown in the table below.

Alternatives to ER Care

The current market trend in retail medicine puts a focus on growth in the urgent care space. According to the research firm Pitchbook, more than $3 billion in private equity and venture capital has been invested in new urgent care clinics since 2010. Many analysts believe this has to do with the new metallic plans that offer cheaper monthly premiums in exchange for higher deductibles. Consumers that choose this option are looking for the lowest monthly price and will monitor their costs by self-selecting urgent-care clinics. It is amazing to see the impact of patient choice coupled with market incentives. When the consumer can make their decision, on their own “dime”, they are voting with their pocketbook and choosing the less expensive option.

This trend probably does not bode well for the hospitals that own the ERs – but it does lower the aggregate costs of care, which is something we all need to strive to achieve. And, more importantly, it does so without compromising the quality. Studies show that retail and urgent care facilities offer better quality for their limited scope of services. It stands to reason if you specialize in a procedure, and perform it many times a day then you become very skilled at it. You also manage to offer that quality service at the lowest price.

Additional to cost considerations, patients usually obtain faster medical care at retail settings than they do at either the ER of their primary care doctor. I relate to this inconvenience. Last year I had to wait six months to book my physical at my physician – and I have been with him for five years.

One interesting consideration is that retail medicine facilities stress to their patients the importance of following up with their primary doctor after a visit. I am unaware of any studies that show if these follow-ups are happening – but I doubt it. The same reason that has consumers choosing the lower-priced, faster-serviced option is probably the same one that prevents them from “paying twice” and duplicating effort.

A Smart Venture for Health Plans

Starting in late 2014, GuideWell, a Florida-based heath insurance company with 1/3rd of the market, created a joint venture with Jacksonville-based urgent care center operator Crucial Care. The goal was to develop a chain of GuideWell Emergency Doctors urgent care facilities. One that just launched is a flagship $22 million facility in Winter Park, Florida, located in a retail center with a Trader Joe’s. The 7,500-square-foot building has 15-20 exam rooms and the ability to handle major medical issues — such as heart attacks, strokes, and internal injuries. It also takes care of minor issues like respiratory illnesses, ear and eye infections and sports injuries.

The team at imagine.GO applauds Crucial Care and GuideWell for this innovative effort. It is a good move following on the heels of Optum, a UnitedHealth Group company, which has opened Optum Clinic Urgent Care facilities nationwide.

The team at imagine.GO applauds Crucial Care and GuideWell for this innovative effort. It is a good move following on the heels of Optum, a UnitedHealth Group company, which has opened Optum Clinic Urgent Care facilities nationwide.

The economics of this business model is smart. A health plan could save millions by offering their newly acquired Exchange members a place to exercise choice in care at a lower cost facility. For example, it costs about $94 to treat a sore throat at an urgent care center compared with the same treatment at the ER costs five times that amount. This difference saves the plan money and the consumer – a win-win. Because of this fact, we assume (and hope) that the GuideWell Emergency Doctors locations are central to areas of high market penetration for the health plan.

This level of investment seems to be on par with the health insurer’s running model of building premium retail health facilities. Correspondingly, many of the GuideWell Retail Centers are around 5000 square feet and are located in premium outdoor malls as freestanding structures. GuideWell was one of the pioneers in the retail insurance space. They now have a whopping 18 of retail storefronts. Understand, these retail settings are quite expensive. Pretty “high-cotton” as my father would say.

Given the cost of this endeavor, the health plan GuideWell must see a strong return on investment in the urgent care model. For full disclosure, I was the Chief Innovation Officer at GuideWell at the time of the retail store model’s inception, having just come off of helping launch a few hundred convenient care clinics for various companies like RediClinic, SmartCare, and The Little Clinic. I was also the founder and first President of GuideWell, so I have a great affection for this company. However, at the time, I advocated for smaller health insurance stores, and even seasonal pop-up stores, because the economics did not support the larger, permanent settings. Here again, we assume (and hope) the numbers are beneficial to our friends at GuideWell. The 2015 individual enrollment should be out soon, so we plan to see if the store expansion and size have worked to their advantage.

However, adding large format flagship stores is contrary to the current trend of building more moderately sized and often semi-permanent insurance stores. We should know, imagine.GO has helped design and build many of them for companies like large blue plan of Tennessee, HMSA, United Healthcare, Affinity Health Plan, and others. We believe in the retail health model and will be writing much more on the trends and innovations in this space very soon.

One other thing we cannot get our heads around is why the GuideWell Emergency Doctors urgent care centers did not take the blue name like their retail insurance store counterpart. The name GuideWell, while a good one, does not have the market awareness like “blue” We assume it must be a restriction of the parent blue brand (in fact they told us we cannot mention the brand in any way or form in this post). In any case, it seems to us like a missed opportunity. Building brand equity takes time and costs a lot of money.

Furthermore, the GuideWell name does not help the health insurance plan acquire business from its competitors in markets where an affiliated urgent care center exists. Consider the affinity consumers could have when they have a health insurer they like and a care facility they like, and they are integrated. It seems to work for Kaiser Permanente, the highest rated health insurer in the country. The health plan and care provider are once again the highest ranked for customer satisfaction in California according to the J.D. Power 2014 U.S. Member Health Plan Study. This is the seventh consecutive year they have received this honor. We at imagine.GO hate to second-guess, but on this one, we simply disagree with the naming decision.

Further Innovation in the Model

So how else is the retail medicine model changing? In a recent interview by Matthew Holt for The Healthcare Blog, Wal-Mart discussed their business model pivot in this space to a new Walmart-owned and controlled “Wal-Mart Care Clinic”.

Traditionally, Wal-Mart hosted what they called the “Clinic at Wal-Mart”. This business model involved Walmart leasing space in the front of their Wal-Mart Supercenters to a clinic operator, in many cases with a health system as part of the venture. With RediClinic, I was involved in the first ever retail clinics built in a Wal-Mart. Since that time, they have had many partners in locations across the country.

Because Wal-Mart owns the clinics now, they control the price and scope of the services they offer. The price is $4 for employees and dependents on the company’s health plan. For customers, the price is $40. The scope of services includes the standard fair for retail clinics, plus basic chronic condition management services, such as treating patients with uncomplicated diabetes, high blood pressure, and similar conditions. They also offer full point-of-care labs. To build and manage these clinics Wal-Mart partners with QuadMed.

Here is a helpful video that explains this new model:

“We believe there’s a significant opportunity to serve the chronic patient and that we have a lot of the offerings that they would need to be successful in managing that chronic condition together with our pharmacy and the over-counter offerings available in the Walmart store.” Ben Wanamaker, Senior Manager of Strategy and Operations at Walmart’

We at imagine.GO speculate the main reason for building these new clinics is due to the high cost of healthcare for their employees. First, in states that opted out of Medicaid expansion, Wal-Mart workers may not be able to get subsidies for their health exchange plans. Under the Affordable Care Act, subsidies start for those making over $15,900 a year. This fact means their workers will have to pay more out-of-pocket, which they cannot afford.

In a board memo leaked to the press, it was revealed that Wal-Mart workers “are getting sicker than the national population, particularly in obesity-related diseases”. These ailments include diabetes and coronary artery disease. The memo also stated that Wal-Mart workers tended to overuse emergency rooms and underuse prescriptions and doctor visits. To put this in perspective, Wal-Mart spends $1.5 billion a year on health insurance. Wal-Mart also announced its health costs were expected to increase by $500 million in 2014 due to its workers signing up for its health-insurance benefits at a higher rate than expected.

In Conclusion

Each of these two interesting pivots on the retail medicine model represents a sensible shift to a now-proven disruption.

The first is from Wal-Mart. They now own health care clinics and can “roll back prices” like they do with everything else. The second is with GuideWell Emergency Doctors. They are looking to steer health plan members to lower health care costs and create savings for the overall health plan.

So whether born out of customer demand or internal cost pressure, both business model pivots look like smart market opportunities. However, the team at imagine.GO feels the GuideWell Emergency Doctors model misses out on the opportunity to drive demand for the health plan due to its naming decision. But either way, we applaud both innovative efforts and look forward to seeing them each succeed in:

1. Improving consumer experience yielding an informed decision maker aligned to their risk and reward;

2. Increasing access to necessary care through an engaged delivery system; and

3. Reducing the aggregate cost of care, with a market-driven, balanced incentive and reward model.

To your health,

The Team at imagine.GO

Sources

The Rise of Retail Clinics: Greenough

http://www.greenough.biz/2013/01/the-rise-of-retail-clinics.html

Retail Medicine Gobbles Up Empty Space In Shopping Center Storefronts: Bloomberg News

http://triblive.com/business/headlines/7480153-74/care-clinics-percent#axzz3NmhYtbrz

Immediate Medical Care: ER or Other Options?: BlueCross BlueShield Association

http://www.bcbs.com/why-bcbs/immediate-medical-care/alternatives-to-emergency.html

UnitedHealth to open Optum Clinic Urgent Care facilities in Houston

http://www.bizjournals.com/houston/news/2014/01/17/unitedhealth-to-open-optum-clinic.html

Big Box Health Care: Are You Ready for Walmart Care Clinics?: Coombs

GuideWell Health launches GuideWell Emergency Medicine Doctors in Orlando

http://www.guidewell.com/guidewell-health-launches-guidewell-emergency-medicine-doctors-in-orlando/

Florida Blue to open urgent-care center near Winter Park Trader Joe’s: Fulker

http://www.bizjournals.com/orlando/blog/2014/04/florida-blue-to-open-urgent-care-center-near.html

Kaiser Permanente California Ranks Highest in J.D. Power Member Satisfaction Study

Health Insurance Companies Get in Shape for 2014: Abelson

Walmart Health Insurance Could Leave A Really Sick Worker Broke: Sherman

Wal-Mart Memo Suggests Ways to Cut Employee Benefit Costs: Greenhouse

http://www.nytimes.com/2005/10/26/business/26walmart.ready.html

Express Urgent Care

http://www.express-urgentcare.com/about-express-urgent-care-walk-in-clinic-in-blaine-mn/

RediClinic Retail Clinics

https://plus.google.com/107742586747331655362/about

Walmart Care Clinic